Covered Call Delta Strategy: Precision Pricing for Optimal Strike

Learn how to use Delta (Δ) to select the optimal strike price for covered calls. Discover how to balance premium income and assignment risk to maximize return.

INVESTMENT STRATEGY

Ben T.

10/7/20255 min read

Introduction: Why Delta Is the Covered Call Trader’s Secret Weapon

The covered call strategy is one of the most powerful tools in an investor’s arsenal. It allows you to generate consistent income—often referred to as “rental income”—from stocks you already own. But while many investors understand the basic mechanics, few master the art of precision strike selection.

That’s where Delta (Δ) comes in.

Delta is more than just a Greek letter—it’s a probability engine that helps you choose the right strike price based on your goals. Whether you're aiming for maximum short-term income or long-term stock retention, Delta gives you the data-driven edge to make smarter decisions.

Here is your comprehensive guide to leveraging Delta for high-yield covered call execution.

What Is Delta (Δ) in Options Trading?

Delta measures how much an option’s price will change for every $1 move in the underlying stock. But for covered call writers, Delta is even more valuable as a proxy for probability.

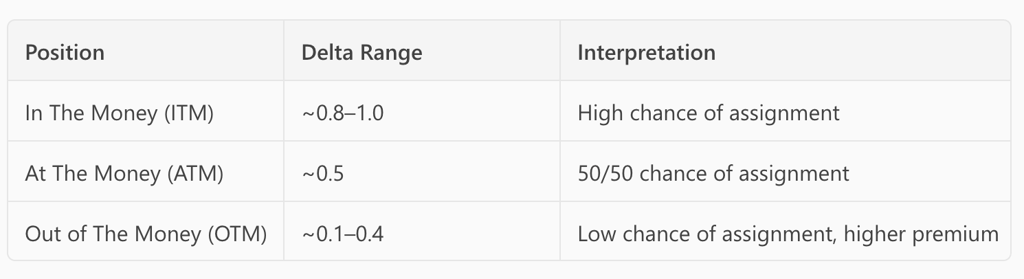

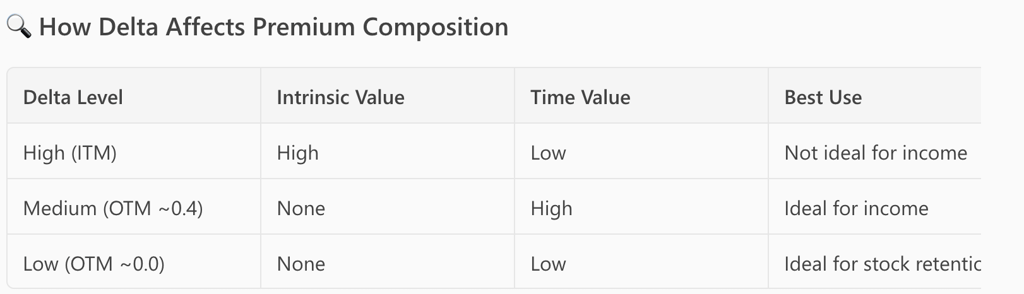

Delta Ranges and Their Meaning

For example, a call option with a Delta of 0.426 implies a 42.6% chance of finishing ITM. For the covered call writer, this is the ultimate tool for precision pricing, as it allows you to quantify the risk of assignment (the risk that your stock will be automatically sold) versus the reward of the premium received.

Why Delta Matters for Covered Calls

Covered calls involve selling a call option on a stock you already own. The goal is to collect a premium while either:

Keeping the stock (if the option expires worthless), or

Selling the stock at a profit (if the option is exercised).

Delta helps you quantify the risk of assignment and maximize the premium you receive.

Strike Price Selection Based on Delta

Choosing the correct strike price is critical to the covered call strategy. The decision rests entirely on your primary goal: maximum short-term income or maximum long-term stock preservation

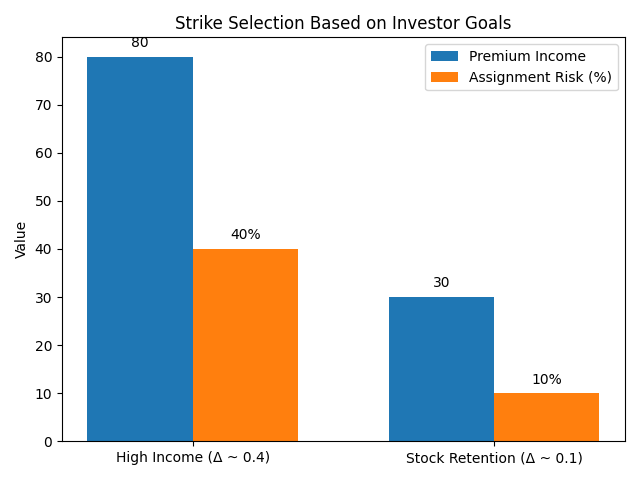

🎯 Goal 1: Maximize Income (Short-Term Bias)

If your goal is to generate maximum yield (income) and you are comfortable with the possibility of your stock being called away (assigned), you should target strikes with a Delta as close to 0.4 (40%) as possible

✅ Why 0.4 Delta Works:

A Delta around 0.4 strikes the optimal balance: it is sufficiently far out-of-the-money (OTM) to collect a solid premium (as OTM options are mostly composed of profitable time value), while having a high enough probability (around 40-45%) of finishing ITM

High premium due to time value.

Moderate assignment risk (~40–45%).

Capital gains if the stock is called away.

Example:

AT&T stock trading at $29.57.

You sell a $30 call with a Delta of 0.426.

Potential annualized return: 37.3%.

This setup gives you the best of both worlds—premium income and upside potential.

🛡️ Goal 2: Preserve Stock (Long-Term Bias)

If you are a long-term investor whose priority is to hold onto the stock at all costs (e.g., to continue benefiting from dividends and long-term appreciation), you must select strikes that are highly unlikely to be hit.

In this scenario, the smart decision is to pick a strike price with a Delta that is as close to zero as possible

✅ Why Low Delta Works:

Minimal assignment risk.

Smaller premium, but consistent.

Stock retention for long-term growth.

Example:

Selling a call with a Delta of 0.025 means only a 2.5% chance of assignment.

Perfect for conservative investors who want to supplement dividends without losing their shares.

Understanding Premiums: Intrinsic vs. Time Value

When writing covered calls, you receive the option's price, known as the premium. This premium consists of two components: Intrinsic Value and Time Value (Extrinsic Value).

Intrinsic Value: The difference between the stock price and strike price (only for ITM options).

Time Value (Extrinsic Value): The value based on time until expiration and volatility.

Delta helps you navigate where the value of the option is concentrated:

1. High Delta (ITM options): These strikes are dominated by Intrinsic Value (the difference between the underlying price and the strike price). Since ITM options are very likely to be exercised, they offer barely any extrinsic value (premium) to the writer. Writing deep ITM options is not considered a smart move for covered call writers focused on income.

2. Low Delta (OTM options): These strikes have zero intrinsic value. Therefore, the entire premium you collect comes from Time Value

By choosing strikes with a Delta around 0.4, you ensure you are writing an OTM option that maximizes the time value you collect, which directly lowers your effective cost basis in the underlying stock. Every premium collected reduces your cost basis, allowing you to withstand larger capital losses in a down market

Combining Delta with Theta (Time Decay)

While Delta helps you select the right price, Theta ($\Theta$), or time decay, governs the optimal timeframe

⏳ What Is Theta?

Theta measures how much an option’s value decays each day as it approaches expiration. For sellers, this decay works in your favor.

📅 Optimal Expiry Window: 30–45 Days

Maximizes time value.

Accelerates decay in final 30 days.

Allows frequent income generation.

By combining the precision of Delta (selecting the right price point) with the power of Theta (selecting the right time frame), you maximize the consistent monthly cash flow you extract from your stock portfolio.

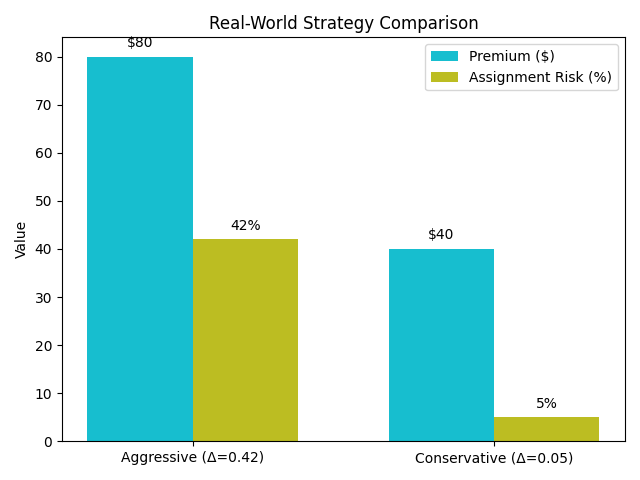

Real-World Strategy Examples

💼 Example 1: Aggressive Income Strategy

Stock: Intel (INTC) at $35

Strike: $36 call with Delta 0.42

Premium: $0.80

Expiry: 30 days

Outcome:

If stock stays below $36 → keep premium + stock.

If stock rises above $36 → sell at profit + keep premium.

🧱 Example 2: Conservative Dividend Strategy

Stock: Johnson & Johnson (JNJ) at $160

Strike: $170 call with Delta 0.05

Premium: $0.40

Expiry: 45 days

Outcome:

Very low chance of assignment.

Premium supplements dividend yield.

Common Mistakes to Avoid

Selling ITM Calls: Limits upside and offers low premium.

Ignoring Delta: Leads to random strike selection.

Using Long Expiry (>60 days): Slower time decay, less frequent income.

Writing Calls on Volatile Stocks: Increases assignment risk and unpredictability.

FAQs: Covered Calls and Delta

Q: Can I use Delta in retirement accounts?

Yes, many IRAs allow covered calls with Level 1 options approval.

Q: What if the stock drops?

You still keep the premium, which cushions the loss. Your cost basis is lowered.

Q: How often should I write covered calls?

Monthly or bi-monthly is ideal. Avoid overtrading—focus on quality setups.

Conclusion: Precision Pays Off

The beauty of using Delta for strike price selection is that it removes guesswork and emotional decision-making. Whether you’re chasing yield or protecting your portfolio, Delta gives you the clarity to act with confidence.

If you are aiming for explosive cash flow, lean towards the 0.4 Delta strike, accepting the higher risk of assignment. If you are prioritizing the long-term health of your capital gains, choose a Delta close to zero

By combining Delta with Theta, you unlock the full potential of covered calls and transform your stock holdings into passive income generators, ensuring you earn money even if the market moves sideways, which is its default state the majority of the time.

Note: Need a reliable well-known broker to trade options: Try TTTrade