How to Build a Diversified Investment Portfolio

Diversified Portfolio: A Complete Guide for Beginners

PORTFOLIO MANAGEMENT

Ben T.

6/23/20255 min read

How to Build a Diversified Investment Portfolio: A Complete Guide for Beginners

Building a diversified investment portfolio is like constructing a sturdy house - you need a solid foundation, quality materials, and a well-thought-out plan. Whether you're just starting your investment journey or looking to refine your existing strategy, understanding portfolio diversification is crucial for long-term financial success.

What Is Portfolio Diversification?

Portfolio diversification is the practice of spreading your investments across different asset classes, sectors, and geographical regions to reduce risk. Think of it as the financial equivalent of "not putting all your eggs in one basket." When you diversify properly, you create a safety net that helps protect your wealth when some investments underperform.

The core principle behind diversification is that different investments often move in opposite directions. When stocks are falling, bonds might be rising. When domestic markets struggle, international markets might thrive. This negative correlation helps smooth out the bumps in your investment journey.

Why Diversification Matters: The Risk-Return Balance

Every investment carries risk, but diversification helps you manage that risk without sacrificing potential returns. Here's why it's essential:

Risk Reduction: A diversified portfolio typically experiences less volatility than individual investments. While you might miss out on the highest possible gains from a single winning stock, you also avoid devastating losses from putting everything into one failing investment.

Consistent Performance: Diversified portfolios tend to deliver more predictable returns over time. This consistency is particularly valuable for long-term goals like retirement planning.

Peace of Mind: Knowing your portfolio can weather various market storms helps you sleep better at night and stick to your investment plan during turbulent times.

Core Asset Classes for Diversification

Understanding the main asset classes is fundamental to building a diversified portfolio. Each serves a different purpose and behaves differently under various market conditions.

Stocks (Equities)

Stocks represent ownership in companies and typically offer the highest long-term growth potential. Within stocks, you can diversify by:

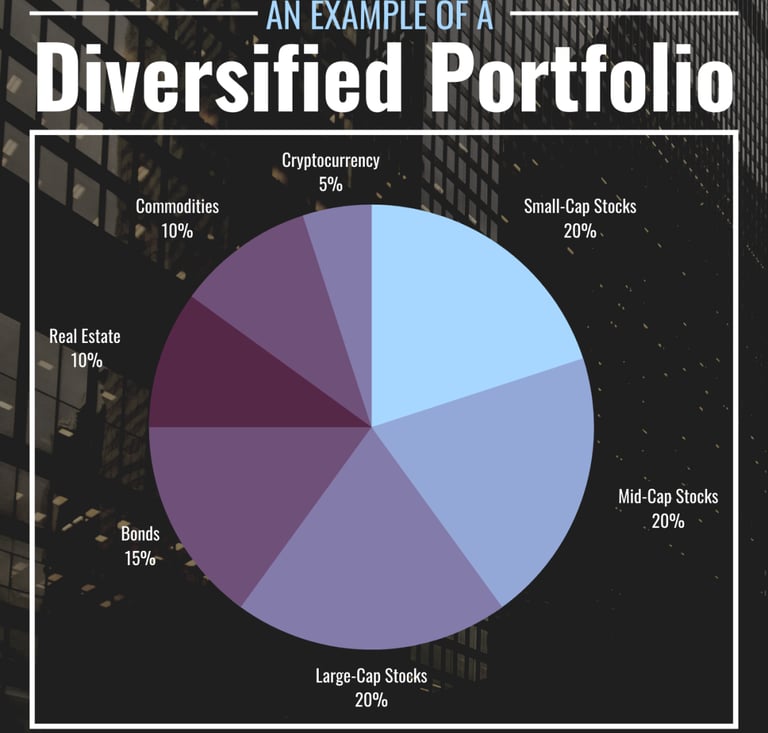

Company Size: Large-cap stocks (established companies), mid-cap stocks (growing companies), and small-cap stocks (emerging companies)

Sectors: Technology, healthcare, finance, consumer goods, energy, and more

Geography: Domestic stocks, developed international markets, and emerging markets

Investment Style: Growth stocks (companies expected to grow rapidly) and value stocks (undervalued companies with solid fundamentals)

Bonds (Fixed Income)

Bonds are loans you make to governments or corporations in exchange for regular interest payments. They typically provide steady income and help stabilize your portfolio during stock market downturns. Bond diversification includes:

Government Bonds: U.S. Treasury bonds, municipal bonds, and international government bonds

Corporate Bonds: Investment-grade and high-yield corporate bonds

Duration: Short-term, intermediate-term, and long-term bonds

Real Estate Investment Trusts (REITs)

REITs allow you to invest in real estate without buying property directly. They provide exposure to commercial real estate, residential properties, and specialized sectors like healthcare facilities or data centers.

Commodities

Commodities include physical goods like gold, oil, agricultural products, and industrial metals. They often perform well during inflationary periods and can provide portfolio protection against currency devaluation.

Cash and Cash Equivalents

While cash doesn't grow significantly, it provides liquidity and stability. Money market funds, high-yield savings accounts, and short-term certificates of deposit fall into this category.

Strategic Asset Allocation: Building Your Foundation

Asset allocation is the process of deciding what percentage of your portfolio to invest in each asset class. This decision has more impact on your returns than individual investment selection.

Age-Based Allocation Rules

The traditional rule of thumb suggests subtracting your age from 100 to determine your stock allocation percentage. For example, a 30-year-old might allocate 70% to stocks and 30% to bonds. However, modern approaches often recommend more aggressive allocations due to longer life expectancies and low interest rates.

Risk Tolerance Assessment

Your comfort level with market volatility should guide your allocation decisions. Consider these factors:

Time Horizon: Longer investment periods allow for more aggressive allocations

Financial Goals: Retirement savings might warrant different allocations than emergency funds

Personal Comfort: Your ability to sleep soundly during market downturns matters

Sample Portfolio Allocations

Conservative Portfolio (Low Risk):

40% Stocks (20% domestic, 15% international, 5% emerging markets)

50% Bonds (30% government, 20% corporate)

10% REITs and alternatives

Moderate Portfolio (Medium Risk):

60% Stocks (35% domestic, 20% international, 5% emerging markets)

30% Bonds (15% government, 15% corporate)

10% REITs and alternatives

Aggressive Portfolio (High Risk):

80% Stocks (45% domestic, 25% international, 10% emerging markets)

15% Bonds (10% government, 5% corporate)

5% REITs and alternatives

Practical Implementation Strategies

Dollar-Cost Averaging

Instead of investing a lump sum all at once, dollar-cost averaging involves investing fixed amounts regularly over time. This strategy reduces the impact of market timing and helps smooth out purchase prices.

Index Funds and ETFs

For beginners, low-cost index funds and exchange-traded funds (ETFs) offer instant diversification within asset classes. A total stock market index fund, for example, gives you exposure to thousands of companies in a single investment.

Target-Date Funds

These funds automatically adjust their asset allocation as you approach your target date (typically retirement). They start aggressive and become more conservative over time, handling rebalancing for you.

Rebalancing Your Portfolio

Over time, successful investments will grow larger while others shrink, throwing off your target allocation. Rebalancing involves selling overweight positions and buying underweight ones to return to your target allocation. Consider rebalancing annually or when allocations drift more than 5% from targets.

Common Diversification Mistakes to Avoid

Over-Diversification: Owning too many similar investments can dilute returns without meaningfully reducing risk. Quality over quantity matters.

Home Country Bias: Many investors overweight their domestic market. International diversification is crucial for true risk reduction.

Sector Concentration: Working in technology and investing heavily in tech stocks creates dangerous concentration risk.

Ignoring Correlation: Some investments that seem different actually move together during market stress. Research correlations between your holdings.

Emotional Rebalancing: Avoid making dramatic changes based on recent market performance. Stick to your long-term plan.

Getting Started: Your Action Plan

Assess Your Situation: Determine your risk tolerance, time horizon, and financial goals

Choose Your Approach: Decide between DIY investing, robo-advisors, or professional management

Start Simple: Begin with broad index funds covering major asset classes

Automate Contributions: Set up automatic investments to maintain discipline

Monitor and Adjust: Review your portfolio regularly but avoid overreacting to short-term market movements

The Long-Term Perspective

Building a diversified portfolio isn't about maximizing returns in any single year - it's about creating a robust foundation for long-term wealth building. This philosophy is shared by many of the world's most successful investors.

Ray Dalio's All Weather Portfolio: The founder of Bridgewater Associates, one of the world's largest hedge funds, developed the famous "All Weather" portfolio specifically designed to perform well across different economic conditions. Dalio's approach consists of 55% U.S. bonds, 30% U.S. stocks, and 15% hard assets (gold and commodities). As the name suggests, the All Weather Portfolio is designed to be able to "weather" any storm using asset class diversification based on seasonality to limit volatility and drawdowns.

What makes Dalio's approach particularly valuable for beginners is its emphasis on risk parity - balancing risk contribution rather than just dollar amounts across asset classes. The aim of Bridgewater's All Weather Portfolio is to use diversification as a tool to smooth returns and lower drawdowns, ensuring that asset classes don't move in tandem.

The Buffett Perspective: While Warren Buffett famously stated, "Diversification is protection against ignorance. It makes little sense if you know what you are doing," this quote is often misunderstood. This perspective highlights his belief that a focused portfolio of well-understood, high-quality investments can outperform a widely diversified one. However, for most individual investors who lack Buffett's decades of experience and research capabilities, proper diversification remains the prudent approach.

Academic Evidence: Modern Portfolio Theory, developed by Nobel Prize winner Harry Markowitz, mathematically proves that diversification can reduce risk without sacrificing expected returns. This isn't just theory - it's been validated by decades of market data showing that diversified portfolios provide superior risk-adjusted returns over time.

Markets will fluctuate, economic cycles will come and go, but a well-diversified portfolio positions you to weather these storms while capturing long-term growth. The key insight from successful investors is that diversification should be viewed as insurance for your wealth, not a limitation on your returns.

Remember that diversification is not a one-time event but an ongoing process. As your life circumstances change, your portfolio should evolve too. The key is starting with solid fundamentals and remaining disciplined in your approach.

Your investment journey doesn't have to be perfect from day one. The most important step is starting, and you can refine your strategy as you learn and grow. With patience, discipline, and proper diversification, you're well on your way to building lasting wealth.