Options Greeks Decoded: Intrinsic Value, Theta & Vega Explained

Unlock option pricing secrets. Learn Intrinsic Value, Time Decay (Theta), and Volatility (Vega) using simple analogies. Master the core components of every option premium.

OPTIONS TRADING

Ben T.

10/15/20259 min read

Deciphering the DNA of an Option: Intrinsic Value, Theta (), and Volatility (Vega ) Explained

For many new investors, options trading feels intimidating—a complex world of Greek letters and unpredictable risks. However, options are merely contracts that give the holder the right, but not the obligation, to buy or sell an asset at a specific price before a fixed date.

Understanding what makes an option contract valuable is the first crucial step toward turning it from a scary concept into an intelligent investor's best friend.

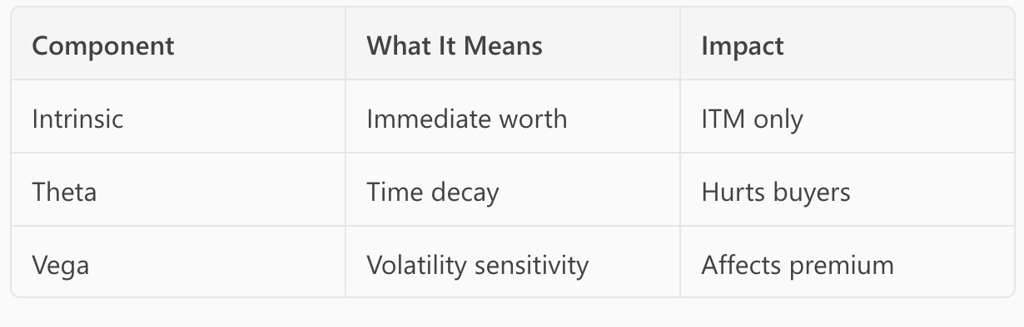

The price you pay for an option is called the premium. This premium is the sum of two fundamental components: Intrinsic Value (the real, immediate worth) and Time Value (the implied, future worth). These values are constantly influenced by three primary "Greeks"—Delta (Δ), Theta (Θ), and Vega (ν).

We’re going here to decipher the DNA of an option (Options Greeks) by breaking down these core concepts into clear, simple terms.

Why Understanding Option DNA Matters for Your Portfolio

Options are highly leveraged tools. A minor percentage move in a stock’s price can translate to a magnified percentage change in the option’s price. This leverage, if misused, can make options feel like a "financial weapon of mass destruction".

However, when used correctly—with discipline and sound investment principles—options can reduce overall investment risk and accelerate your wealth building.

Mastering the three components of option value allows you to:

1. Price Trades Accurately: Understand if an option is expensive or cheap relative to its risk.

2. Manage Risk: Determine your maximum profit and maximum loss scenarios with pinpoint accuracy.

3. Generate Income: Utilize concepts like time decay (Theta) to consistently earn cash flow, particularly when selling options, as in the Covered Call strategy

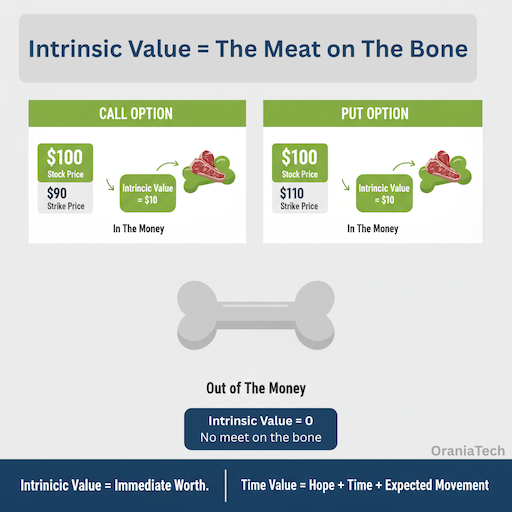

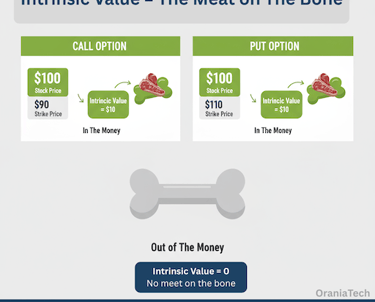

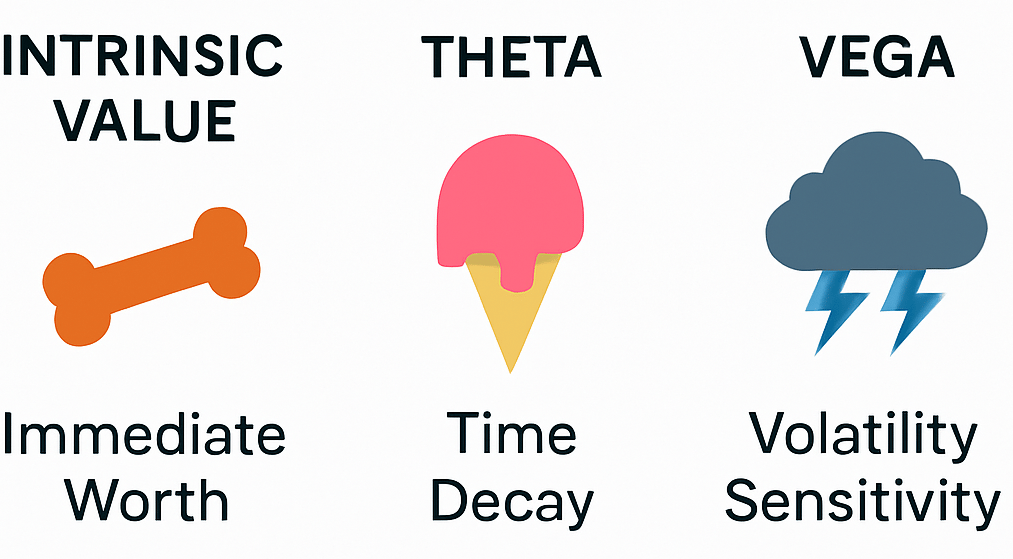

Component 1: Intrinsic Value—The "Meat on the Bone"

Quick definition: Intrinsic Value (IV) is the real value of an option. It represents how much immediate profit an option buyer would realize if they exercised the contract right now.

If an option has Intrinsic Value, it is considered In The Money (ITM). If an option cannot be profitably exercised immediately, it has zero intrinsic value.

The Analogy: The "Meat" of the Deal

Imagine you buy a contract (a Call Option) to purchase a specific stock for $90. The stock is currently trading at $100.

The moment you buy the contract, it is instantly worth: $100 (Current Stock Price)−$90 (Strike Price)=$10 of Intrinsic Value This $10 is the "meat on the bone"—the immediate, measurable value inherent in the option.

Intrinsic Value in Calls vs. Puts

The definition of "In The Money" (ITM) flips depending on the type of option:

• Call Option: A call is ITM if the stock price is above the strike price. Call options with a higher Intrinsic Value will have a Delta () closer to 1 (100%), meaning the option price moves almost dollar-for-dollar with the stock price.

• Put Option: A put is ITM if the stock price is below the strike price. Puts gain Intrinsic Value when the underlying asset moves lower than the strike price.

If an option is Out of The Money (OTM), meaning exercising it would result in a loss, the Intrinsic Value is mathematically negative. Since options cannot have negative values, OTM options always have zero intrinsic value

Example (simple math):

Stock = $100; Call strike = $90 → $10 intrinsic (and the rest of the premium is time value).

Stock = $100; Put strike = $110 → $10 intrinsic.

Takeaway: Intrinsic value = immediate worth; Time value = hope + time + expected movement. At expiration, all time value disappears—only intrinsic remains.

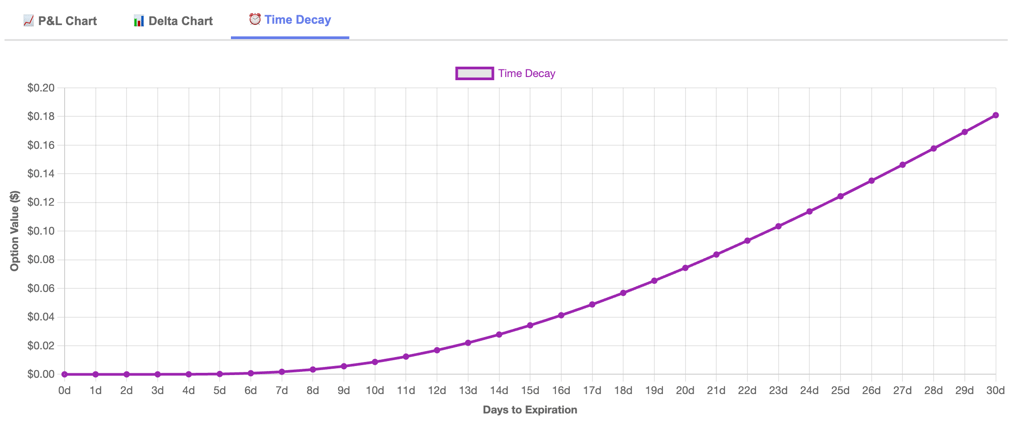

Component 2: Time Decay (Theta ): Your Premium’s Expiration Date

If an option has zero Intrinsic Value (meaning it's OTM), its entire price consists of Time Value, also known as Extrinsic Value.

The Analogy: Time Value as "Hope"

Time value represents the uncertainty and hope that the stock price will move in the necessary direction before the contract expires. The longer an option has until expiration, the more time there is for the underlying asset to move into a profitable position, thus increasing its Time Value.

Here are Everyday analogies:

Melting ice cream: tasty at first, but the closer you get to the sun (expiration), the faster it melts.

Expiring coupon: valuable when you’ve got weeks to use it; near the deadline it’s worth less by the day.

This aligns with how time value shrinks as expiry approaches.

The Concept: Time Decay (Theta )

The value lost simply due to the passage of time is called Time Decay, or Theta ().

• Definition: Theta measures how much the option premium loses value each day it approaches expiry.

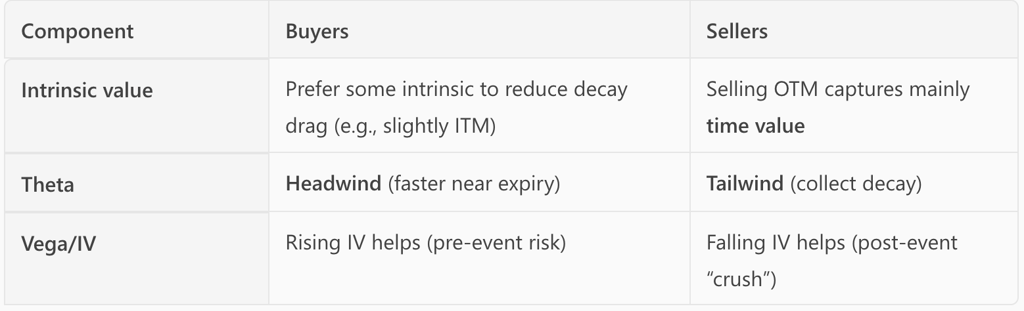

• Options Seller's Advantage: As an options seller (or writer), time decay is your friend. You receive the premium upfront, and you want the option to expire worthless (OTM) so you keep the entire premium.

• Options Buyer's Disadvantage: If you buy an option, Theta works against you, constantly eroding your investment's value.

The Acceleration of Time Decay

Crucially, time decay is not linear.

Theta decay accelerates sharply once the option moves within 30 days of expiry. This means:

• For Sellers (Covered Calls): The optimal window for writing covered calls is the 30-45 day window. This timeframe captures sufficient Time Value in the premium while allowing the option seller to benefit from the accelerating decay as the option nears expiration.

• Practical Example (Expiring Coupons): An option's time value is like a coupon for a big discount. The day the coupon is issued, it holds great value. But as the expiration date nears, especially in the last few weeks, the coupon loses its perceived value very quickly because the window to use it is closing.

Buyer implications:

Short‑dated options can look cheap but theta is steep—you need the stock to move enough and fast to outrun decay. Longer‑dated options (e.g., LEAPs) decay slower per day, trading a higher price for more time.

Example of Time Decay with IV50

Component 3: Volatility (Vega ): Measuring Market Uncertainty

Volatility is another critical factor in determining the Time Value component of an option premium. Volatility refers to the degree and force with which an instrument's price moves.

The Concept: Implied Volatility (Sigma ) and Vega ()

The price component related to a stock's expected future movement is Implied Volatility (IV), denoted by the Greek letter Sigma (Σ).

• Definition: IV is a forward projection of how much the market expects the stock to move. A higher IV means the stock is expected to be more volatile, causing wild up and down price swings.

• Vega (): This Greek letter tells you exactly how much the option price will change if the Implied Volatility changes by one percent.

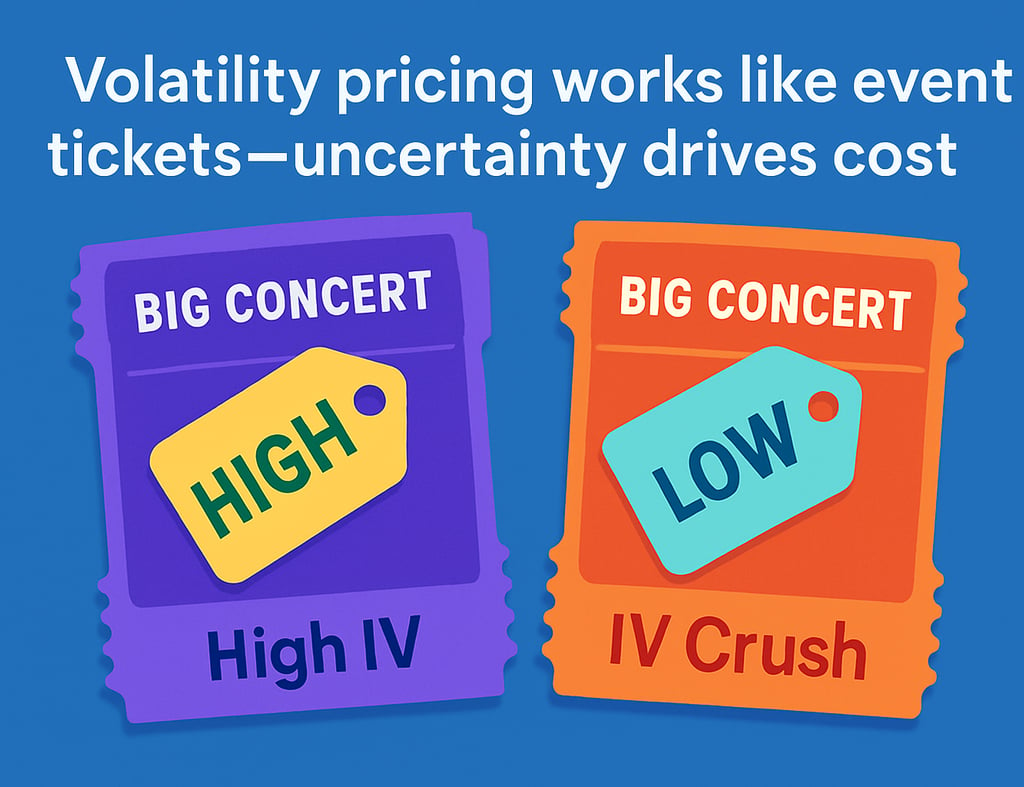

The Analogy: Event Ticket Pricing

Think of volatility like the price surge for tickets to an unpredictable, high-stakes event.

If a company is about to announce the results of a drug trial (a high-volatility event) or publish its earnings report, the market expects massive price movement. This uncertainty increases the option premium significantly.

• High Volatility = Higher Premiums: The difficulty of predicting stock behavior commands a higher price (premium) for the option because of the additional risk/reward it poses. Option writers demand a higher payment for taking on this uncertainty risk.

• Seller's Sweet Spot: Covered call writers look for stocks trading at IV levels between 30% and 70%. Options below this range don't offer enough premium, while those above 70% are too volatile and expose the covered call writer to excessive risk of assignment (having the stock called away)

Who benefits:

Option buyers tend to benefit when IV rises after entry (vega positive).

Option sellers tend to benefit when IV falls (vega negative exposure), particularly for strategies that short extrinsic value.

Putting the DNA Together: Practical Scenarios

The three components (Intrinsic Value, Theta, and Vega) are intertwined in every options contract, determining the final premium and influencing the profit potential.

Scenario 1: The Long-Term Investor (Prioritizing Stock Preservation)

A long-term investor focuses on generating cash flow (synthetic dividends) while ensuring their underlying stock holding is protected.

• Focus: Maximize Theta decay benefit and minimize Vega risk.

• Strategy: Write Covered Calls that are far Out-of-the-Money (OTM), meaning they have zero Intrinsic Value and a low probability of being exercised.

• Precision Pricing: They select strikes with a very low Delta (), often near (2.5% probability of assignment). This approach ensures the seller benefits mainly from Time Value decay (Theta), collecting a smaller premium but almost guaranteeing they keep the stock.

Scenario 2: The Short-Term Income Hunter (Maximizing Yield)

An income-focused trader is willing to risk having their stock called away in exchange for the highest immediate cash premium.

• Focus: Balance the high premiums offered by Time Value with an acceptable risk of assignment.

• Strategy: Write OTM Covered Calls that are close enough to the stock price to carry a decent premium (high time value) but still allow for some profit if assigned.

• Precision Pricing: They target strikes with a Delta () near (40%). This Delta range strikes the optimal balance, maximizing the Time Value collected while keeping the probability of assignment manageable.

Another Practical Example: Covered Call Seller (Income Focus)

You own 100 shares at $50. You sell a 1‑month OTM call at strike $55 for $1.20 per share. If the stock stays below $55, the option likely expires worthless and you keep the premium—a “synthetic dividend” boosted by theta decay. If the stock rises and you’re assigned, your upside is capped at $55 + premium. Sellers often look for liquid names, watch IV, and may prefer ~30–45 DTE to balance premium with manageable risk, adjusting around 21 DTE if needed.

Scenario 3: The Leveraged Buyer (LEAPs Strategy)

The long-term options buyer (such as those using the "Buffett Call" LEAPs strategy) benefits from volatility and time.

• Focus: Maximize Intrinsic Value gains and minimize the negative effect of Theta.

• Strategy: Buy Long-Term Equity Anticipation Securities (LEAPs)—options expiring over a year out.

• Benefit: Because LEAPs have so much Time Value built in, the negative impact of Theta decay is very slow at first. If a major volatility shock (Vega) causes the underlying stock to rise, the LEAP premium will realize a larger gain than a short-dated option due to the higher intrinsic value sensitivity. The trade‑off is higher upfront cost and exposure to broader market swings in IV and rates.

Conclusion: Trading with Confidence

Options contracts are just like any other financial instrument: they are merely a tool. When used correctly, they are instruments of risk management and disciplined income generation.

By understanding the DNA of an option—how Intrinsic Value provides immediate worth, how Theta accelerates time decay in the seller's favor, and how Vega measures price uncertainty—you move beyond guesswork. You gain the power to make rules-based trading decisions, allowing you to profit even when the market is moving sideways, which, as the sources note, is the market's default state the majority of the time.

The knowledge of the Greeks should be used not to overcomplicate the trade, but to simplify decision-making. Focus on stability, adhere to simple rules regarding timeframes (30-45 days) and strike selection (Delta), and you can transform options from a perceived gambling tool into a core component of your intelligent investment strategy

FAQs (Options Greeks Explained)

1) What’s the difference between intrinsic and time value?

Intrinsic value is the immediate ITM amount if exercised now; time value is the extra you pay for time and uncertainty. At expiration, time value becomes zero.

2) Why does theta accelerate near expiration?

Because less time remains for a profitable move, the time value erodes faster in the final weeks—especially for ATM options.

3) How does implied volatility (IV) affect option prices?

Higher IV lifts premiums; lower IV compresses them. Vega shows how much price changes per 1‑point IV move.

4) What is “IV crush”?

A sharp drop in IV (and option premiums) after an anticipated event (e.g., earnings) when uncertainty is resolved. Buyers can lose premium even if price moves modestly.

5) Do long‑dated options always lose less to theta?

Per day, yes—theta is slower for longer‑dated options; you pay more upfront but face less daily decay.

6) Is ~30–45 DTE “best” for selling options?

There’s supporting research for ~45 DTE entries with 21‑DTE management to balance theta collection and gamma risk; still, treat it as a guideline, not a rule.

Disclaimer:

This article is for educational purposes only and does not constitute financial, investment, or trading advice. Options trading involves significant risk and is not suitable for all investors. Always conduct your own research and consult with a qualified financial advisor before making any trading decisions.

Our Preferred Broker: TTrade