From Saving to Thriving: Your First Steps into Investing in Europe

Learn how to start investing in Europe—even with just a few euros. This beginner-friendly guide covers brokers, ETFs, taxes, and smart strategies to grow your wealth step by step. Perfect for EU, EEA, and UK residents.

INVESTMENT STRATEGY

Ben T.

11/7/20258 min read

Your First Steps into Investing: A European Beginner's Guide (2025)

Introduction: Why investing matters in Europe now

If you keep all your money in cash, inflation quietly shrinks its purchasing power over time. In the euro area, headline inflation is estimated at 2.1% (Oct 2025)—close to the ECB target, but still a steady headwind against idle savings. Services inflation remains stickier at 3.4%, reminding us that prices for everyday things can outpace deposit rates. (ec.europa.eu)

At the same time, Europeans are saving a lot: the euro area household saving rate sits around 15.4% (Q2 2025), well above pre‑pandemic norms. That’s great—if those savings are put to work. Otherwise, they risk falling behind the cost of living.

This guide will show you—step by step—how to start investing sensibly in Europe, using everyday examples and pointing to the platforms, rules, and taxes you’ll actually face across the EU/EEA and the UK.

What Exactly Is Investing? (Think of It Like Planting Seeds)

Investing means buying assets—like company shares, bonds, or funds—that can grow in value or generate income over time. Instead of your money sitting still (and shrinking), you're putting it to work: funding businesses, supporting governments, or backing real estate projects.

Think of it like planting seeds. Some grow quickly, others take years, and you'll weather storms along the way. But over the long term, a diversified investment portfolio has historically outpaced cash savings by a significant margin.

Three Compelling Reasons for Europeans to Start Investing Today

1. Beat Inflation and Protect Your Future Purchasing Power

Even moderate inflation is relentless. At 2.1% annual inflation, your money loses about half its purchasing power every 33 years if it just sits in cash. Sensible, diversified investing seeks to outpace inflation and preserve—ideally grow—your wealth over time.

2. Build Toward Retirement and Financial Independence

Compound growth is magical. Regular contributions, even modest ones, can snowball into substantial wealth over decades. Starting early reduces the burden later and gives time the chance to work its magic on your behalf.

3. Make Europe's High Savings Rate Work Harder

With household saving rates elevated at 15.4%, shifting even a portion of that cash into long-term investments can help close Europe's savings-to-investment gap that policymakers keep fretting about. Your personal wealth benefits, and so does the broader economy.

Understanding Brokers: Your Gateway to Investing

A broker (or investment platform) is your regulated middleman—the company that holds your account, executes your trades, and keeps your investments safe. In Europe, these firms operate under strict rules called MiFID II/MiFIR, which ensure investor protection, transparency, and fair pricing.

How to Choose the Right Broker: Your Checklist

✅ Regulation & Investor Protection

EU investment firms must participate in Investor Compensation Schemes that protect you up to a minimum of €20,000 if the firm fails (note: this doesn't protect against market losses, only firm insolvency). Ireland's scheme covers 90% up to €20,000; Germany's does the same.

✅ Product Access

Can you buy UCITS ETFs (the European retail-friendly funds)? What about international stocks and bonds? Check before you commit.

✅ Transparent Costs

Look beyond headline "€0 commission" claims. Compare all-in costs including currency conversion fees, spreads, custody fees, and withdrawal charges.

✅ User-Friendly Features

Fractional shares let you invest small amounts regularly. Automated savings plans remove emotion from investing. German savings plans have fueled a 33% growth in ETF ownership in the past year, making investing accessible to millions.

✅ Best Execution Standards

New EU rules are tightening execution quality and banning payment-for-order-flow (PFOF) by 2026, which means better prices for retail investors like you.

Popular European Platforms (2025)

Here are some widely-used brokers accessible to European residents (always verify they serve your specific country):

Interactive Brokers (IBKR) — Comprehensive global access, professional tools, strong reputation. EU operations consolidated in Ireland, serving EEA clients.

Trading 212 — Broad EU coverage via UK/Cyprus/Germany entities. Check their official supported countries list before opening an account.

Trade Republic — Available across many EU countries (not currently in the UK as of late 2025). Popular in Germany with commission-free savings plans.

Freedom24 — EU-regulated under CySEC, offering stocks, ETFs, bonds, and even US options.

Pro tip: Always open accounts in your real country of residence, verify investor compensation coverage, and compare total costs including FX conversion.

Types of Investments: Your Building Blocks

Stocks (Shares)

Ownership slices of companies. Higher long-term growth potential, but expect roller-coaster volatility along the way.

ETFs (Exchange-Traded Funds)

Think of these as pre-mixed investment smoothies—baskets of stocks or bonds that track an index like the MSCI World or STOXX Europe 600. European ETF assets are approaching €2.3 trillion, with record inflows in 2024. Most retail-friendly European ETFs are UCITS, which come with standardized risk and cost disclosures.

Accumulating vs. Distributing ETFs: Accumulating ETFs reinvest dividends automatically (tax-efficient in many countries), while distributing ETFs pay dividends out to you. Tax treatment varies by country, so check your local rules.

Bonds

Loans to governments or companies that pay interest. European investors flocked to fixed income in 2024-25 as yields rose, making bonds attractive again after years of ultra-low rates.

Real Estate

Direct property ownership or listed Real Estate Investment Trusts (REITs). Sensitive to interest rates and local tax rules.

Cash & Money Markets

Essential for emergency funds. Some brokers offer EUR money-market or "savings plan" options, though watch for fees and product structures.

Thematic/ESG/Active ETFs

Thematic ETFs have found strong resonance among European retail investors thanks to their relatable topics like clean energy, technology, or healthcare. But be cautious—thematic investing can be riskier than broad-market exposure.

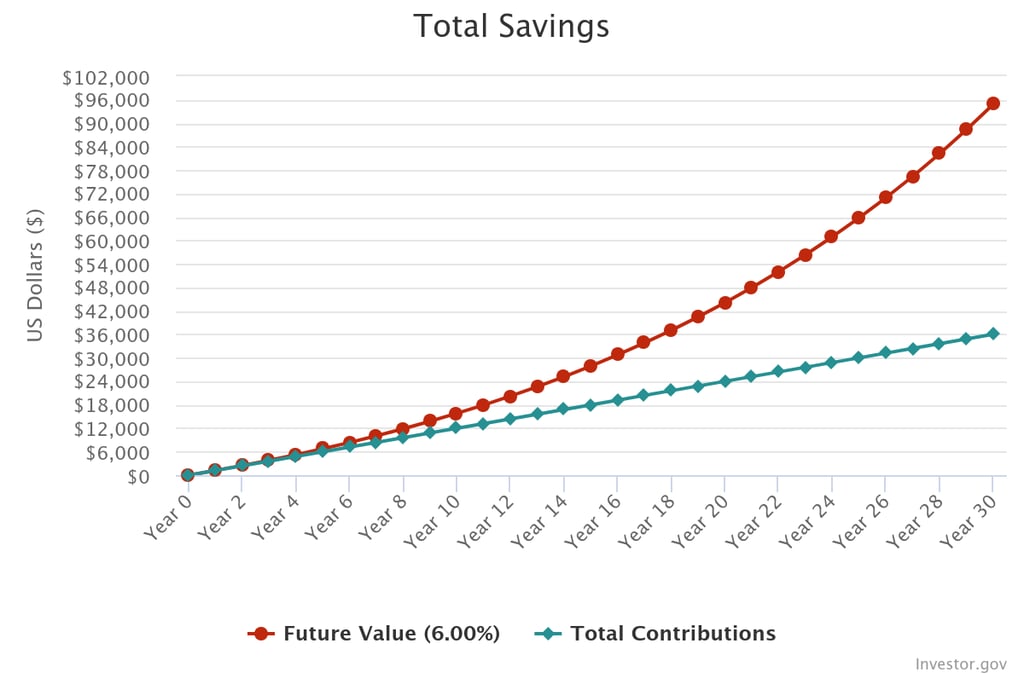

The power of compounding (simple example)

Imagine you invest €100/month at an average 6% annual return:

After 10 years: ~€15,900 contributed → ~€16,300 total

After 20 years: ~€24,000 contributed → ~€46,400 total

After 30 years: ~€36,000 contributed → ~€100,400 total

Your money earns returns; those returns earn returns. The earlier you start, the more compounding works for you.

Risk vs. Reward: What Every Beginner Must Know

Volatility ≠ Permanent Loss

Stock markets can drop 20%+ in bad years and still deliver positive long-run returns. The key word is "long-run." Short-term swings are normal; panic-selling turns paper losses into real ones.

Diversification Is Your Safety Net

Spreading your money across many companies, countries, and asset types lowers the pain of any single investment crashing. Broad ETFs do this automatically.

Behavior Trumps Strategy

A consistent monthly investment plan often beats "waiting for the perfect moment." Markets reward discipline over cleverness.

Regulation Helps (But Doesn't Eliminate Risk)

European reforms—stronger execution policies, PFOF bans, better transparency—are steadily improving the experience for retail investors. But no regulation can protect you from market downturns.

How Much Money Do You Really Need to Start?

Here's the beautiful part: German investors can set up automated monthly investments as low as €1, though typical amounts are closer to €100. Thanks to fractional shares and low-cost brokers, you can begin with tens of euros and automate monthly contributions.

Don't wait until you have thousands. Start small, start today, and let consistency do its work.

Navigating European Tax Rules (The Basics)

Important: This is general information, not personalized tax advice. Always consult a local tax professional or your country's tax authority.

Capital Gains & Dividends Vary Widely

Top marginal capital gains tax rates across Europe range from 0% (Belgium on certain long-held shares) to around 30% (France). Your allowances, holding periods, and local rules matter enormously.

Cross-Border Dividend Tax Is Getting Easier

Historically, claiming treaty rates on dividends from other EU countries meant slow, paper-heavy refunds. The new FASTER Directive introduces a single digital tax residence certificate (issue within 14 days) and fast-track relief, making cross-border investing smoother.

Product Disclosures: EU vs. UK

EU investors: Retail funds provide a PRIIPs Key Information Document (KID) summarizing risks, scenarios, and costs.

UK investors: The FCA is replacing PRIIPs with Consumer Composite Investments (CCI) Product Summaries in the coming years.

Accumulating vs. Distributing ETFs (Tax Angle)

Many EU countries tax dividends annually but capital gains only upon sale. This makes accumulating ETFs potentially more tax-efficient for long-term savers, as they can defer taxes and compound more efficiently. Germany's Vorabpauschale is an exception (deemed distribution), so always check local specifics.

What's Happening in European Retail Investing Right Now

European ETF market flows approached record levels in 2024, with assets nearing €2.3 trillion. Here's what's driving the momentum:

1. Record ETF Adoption

2024 saw all-time-high ETF inflows in Europe, with continued interest into 2025, especially in bonds and US equities (via UCITS ETFs). Moreover, in Q3 2025 alone, the ETF market attracted EUR 1.65 billion - source

2. The Fixed Income Comeback

As interest rates rose, investors rediscovered short-duration bonds and money-market funds.

3. Fractional Investing & Savings Plans

The number of ETF savings plan accounts outside Germany more than doubled from 2023 to 2024. Regulators are working to harmonize fractional share treatment across the EU, making it even easier for beginners to start.

4. Tighter Execution Standards

EU reforms are banning PFOF and raising the bar for best execution—good news for retail outcomes and fair pricing.

Seven Mistakes to Avoid (Learn from Others' Pain)

Going All-In on a Single Stock or Theme

Diversify. Broad ETFs reduce single-bet catastrophic risk.Trying to Time the Market

Perfect timing is a myth. Automate monthly contributions instead.Ignoring Hidden Fees

A "€0 commission" label can hide currency conversion or spread costs. Compare total costs.Using the Wrong Account Type

Ensure your broker is MiFID-regulated with clear investor protection and segregated assets. Check the applicable compensation scheme.Forgetting About Taxes

Keep basic records of purchases, sales, and dividends. The FASTER framework will help with cross-border relief, but you still need to file correctly.Panic-Selling During Downturns

Markets go up and down. Selling in fear locks in losses. Stay the course.Chasing Hot Tips and Trends

When retail flows pour into speculative products, it can be a contrarian signal of market overheating. Stick to your plan.

Your Action Plan: First Steps to Take Today

Step 1: Set Your Foundation

Build an emergency fund (3–6 months' expenses) in cash or high-liquidity instruments. Define your goals—retirement, house deposit, kids' education.

Step 2: Pick a Reputable Broker

Compare Interactive Brokers IE, Trading 212, Trade Republic (check your country), or Freedom24. Confirm regulation, fees, and supported products in your location.

Step 3: Start with a Simple Core

A global equity UCITS ETF (accumulating) + a EUR bond UCITS ETF (short/intermediate duration) can form a robust, beginner-friendly core portfolio.

Step 4: Automate Everything

Set a monthly transfer and buy plan (fractional shares if needed) to remove emotion and benefit from euro-cost averaging. Brokers often waive commissions for savings plans, making them economically attractive.

Step 5: Stay Informed (Not Obsessed)

Read the PRIIPs KID or Product Summary for any fund you buy. Rebalance once or twice a year—no need to watch the market daily.

Localization Tips: EU/EEA vs. UK

EU/EEA Investors:

Expect PRIIPs KIDs for retail funds

FASTER will simplify dividend withholding tax relief via digital certificates and relief-at-source as it rolls out

Many large brokers passport across the EU; Trade Republic is available in numerous EU countries (but not the UK)

Trading 212 supports most EEA markets via its entities—check their live list

UK Investors:

Broker choices differ; Trade Republic isn't in the UK as of late 2025

The FCA is moving to a CCI regime replacing PRIIPs KIDs—so disclosures will look different from EU products

Investor Protection Examples:

Ireland (IBKR IE): ICS covers 90% up to €20,000

Germany (EdW): covers 90% up to €20,000 for eligible investment claims

Final Thoughts: Keep It Boring, Keep It Growing

Investing for Europeans doesn't need to be flashy, complicated, or time-consuming. For most beginners, a simple diversified ETF portfolio, automated monthly contributions, and a long-term mindset are enough.

Europe's regulatory framework—from KIDs to FASTER to best-execution reforms—is steadily making investing more transparent and investor-friendly. The infrastructure is in place. The products are accessible. The only thing missing is your decision to start.

Start small, start today, and let compounding—and time—work their quiet magic.

Your future self will thank you.

Disclaimer: This article is for educational purposes only and does not constitute financial, tax, or investment advice. Always do your own research and consult with qualified professionals before making investment decisions.